16 minute read

AT A GLANCE

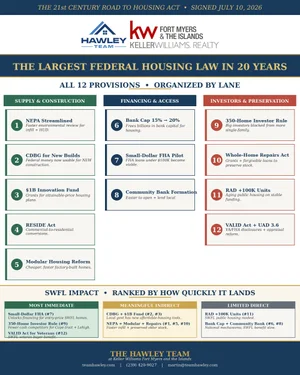

On July 10, 2026, the largest federal housing package in about two decades quietly became law. Congress passed the bipartisan 21st Century ROAD to Housing Act with genuinely overwhelming margins (Senate 85-5, House 358-32). The President did not sign it, but did not veto it. Under the 10-day constitutional window, the bill became law by default. This is not one narrow tweak. It is 12 separate provisions across three lanes: supply and construction, financing and access, and investor and preservation policy. Today's post is the Hawley Team's honest overview of what is actually in the law, translated out of federal-agency acronyms into plain English, and mapped specifically to what each provision may mean for a Southwest Florida buyer, seller, or homeowner. Some provisions will land quickly here. Some are effectively neutral for our market. And a few could meaningfully reshape the specific SWFL submarkets where our team works most (Cape Coral tract homes, Lehigh Acres entry-price inventory, post-Ian rebuild markets, and manufactured home communities). We are also planning a follow-up series of deeper-dive posts across the next two weeks.

How This Became Law (In One Paragraph)

The Senate passed the bill 85 to 5 on June 22, 2026. The House passed it 358 to 32 on June 23, 2026. Those are not partisan margins. Those are near-consensus margins across both parties. The President had 10 days to sign or veto. Under the Constitution, if a bill sent to the President is not signed within 10 days while Congress is in session, it automatically becomes law. That is what happened here. The President neither signed nor vetoed the bill, and the ROAD Act became federal law on July 10, 2026. The Hawley Team takes no political position on why the bill was not signed. The bill is now law, and the practical question for our SWFL clients is what the 12 provisions actually do. We have laid them out below.

The Three Lanes at a Glance

The law is organized around three practical goals. Every one of the 12 provisions falls into one of these three lanes.

Lane 1: Supply and Construction. Get more homes built, faster. Streamline environmental reviews, unlock federal community-development money for new builds, fund innovative construction approaches, convert commercial buildings into housing, and cut red tape for factory-built (modular and manufactured) homes.

Lane 2: Financing and Access. Get more people into homes. Free up bank capital for housing investments, encourage lenders to write small mortgages (under $100,000), and make it easier for local community banks to form and lend.

Lane 3: Investors and Preservation. Rebalance the playing field. Limit large institutional investors from buying single-family homes, provide grants to fix aging homes, expand a program that stabilizes older public housing, and modernize how veterans compare loans and how appraisers value homes.

Lane 1: Supply and Construction

Provision 1. Streamlined NEPA Environmental Reviews

The National Environmental Policy Act requires federal projects to undergo an environmental review before construction. For decades, that review has been one of the biggest sources of delay for federally-supported housing. The ROAD Act shortens the review for HUD-funded projects and for what the law calls "infill" projects (building new homes on empty lots inside existing neighborhoods rather than clearing new land). If a house is going up between two buildings that were already environmentally reviewed, the developer may be able to skip a fresh review entirely.

What this may mean for SWFL. Cape Coral, Fort Myers, Lehigh Acres, and North Fort Myers all have significant infill inventory (empty lots inside otherwise-built neighborhoods). If federal funding is available, those infill lots may see faster construction timelines. Post-Ian rebuild sites on Fort Myers Beach, Sanibel, and Captiva may also benefit where the rebuild uses HUD funding pipelines.

Provision 2. CDBG Funds Unlocked for New Construction

CDBG stands for Community Development Block Grant, the federal money HUD sends to cities and counties each year for community and housing needs. Under prior rules, CDBG money could mostly only be spent repairing existing housing. Under the ROAD Act, that same money can now also be used to build brand-new affordable homes. That is a meaningful change in how local governments can deploy their annual federal allocation.

What this may mean for SWFL. Lee County and Collier County each receive CDBG allocations. The new authority gives local governments a new tool to add affordable inventory. Whether local governments actually use the tool depends on local decisions. We will watch how Lee and Collier respond.

Provision 3. The $1 Billion Innovation Fund

The law authorizes a $1 billion competitive grant program for "attainable" housing (meaning homes priced for middle-income families). Local governments with strong plans apply, and the plans judged the most promising win federal funding. The bill also creates a specific grant program communities can use to develop "pattern books" (collections of pre-approved housing designs that would need fewer approvals before construction).

What this may mean for SWFL. Any Lee or Collier County government or municipal agency with a serious plan for attainable-price inventory can compete for federal money. Cape Coral's utility-expansion program history and Lehigh Acres' entry-price inventory could both be strong platforms for an application.

Provision 4. The RESIDE Act (Commercial-to-Residential Conversions)

The bill funds converting empty commercial buildings (dead strip malls, vacant office buildings, old warehouses) into housing. This is where a significant amount of the underused real estate stock in most American cities lives.

What this may mean for SWFL. The Fort Myers area has meaningful older commercial inventory (older strip retail, some office). North Fort Myers has older commercial along US 41. Lehigh Acres has some. Whether any of these actually convert depends on ownership, financing, and local zoning cooperation. The federal money is now available. The market will decide what actually happens.

Provision 5. Modular Housing Reform

Factory-built housing (both modular homes and manufactured homes) is one of the fastest and cheapest ways to add housing supply. The ROAD Act cuts red tape and production costs for modular and manufactured housing.

What this may mean for SWFL. Manufactured home communities in Lehigh Acres, North Fort Myers, and some Cape Coral areas have real presence. New manufactured home inventory may become cheaper and faster to build post-ROAD. Buyers looking at manufactured home communities as entry-price options should watch this closely.

Lane 2: Financing and Access

Provision 6. Bank Investment Cap Raised From 15% to 20%

Federal banking regulations limit how much of a bank's capital can go to "public welfare investments," which include affordable housing. The prior cap was 15%. The new cap is 20%. That five-point increase frees up billions of dollars of bank capital that can now flow into affordable housing lending and investment.

What this may mean for SWFL. Regional banks that lend heavily in Lee and Collier counties now have more room to invest in affordable housing here. Whether they actually do so is a market decision. But the ceiling that was holding them back has been raised.

Provision 7. Small-Dollar FHA Mortgage Pilot

This is one of the most under-covered provisions in the bill and one of the most consequential for Southwest Florida entry-price buyers.

The problem it addresses: mortgages under $100,000 are historically hard to get. Lenders spend nearly the same time and cost originating an $80,000 loan as they do a $500,000 loan, but they earn far less from the smaller loan. So lenders simply do not offer small-dollar mortgages very often. Buyers looking at homes under $100,000 have often been forced into cash-only purchases or unfavorable loan terms.

The ROAD Act authorizes HUD to establish an FHA small-dollar mortgage pilot program. Under the pilot, HUD can provide direct payments to lenders, technical assistance, and adjusted terms to make it economically viable for lenders to originate mortgages of $100,000 or less. HUD has up to one year to launch the pilot, and it is authorized for four years once launched.

What this may mean for SWFL. Older manufactured homes in Lehigh Acres and North Fort Myers. Some older Cape Coral condos. Some older Fort Myers area homes. All of these sit in price ranges where a small-dollar mortgage could unlock a category of first-time buyers who previously could not get financing. The specific SWFL communities where sub-$100,000 inventory exists could see a meaningful demand shift once the pilot is live.

Provision 8. Community Bank Formation and Lending

The law makes it less complicated to open new small local banks and easier for existing community banks to lend. More local banks in a community typically means more loan options and more relationship-based lending.

What this may mean for SWFL. Community bank presence in Lee and Collier counties is meaningful but not saturated. If the ROAD Act encourages new community bank formation, buyers in specific SWFL submarkets may find more local lending options in the coming years.

Lane 3: Investors and Preservation

Provision 9. Large Institutional Investors Limited From Buying Single-Family Homes

This is the headline provision that has generated the most national coverage. The law restricts the purchase of new single-family homes by large institutional investors defined as any entity that already owns or controls 350 or more single-family homes.

Important details:

No forced divestiture. An investor that currently owns 400 or 4,000 single-family homes does not have to sell any of them. The law only limits future acquisitions.

Build-to-rent exemption. If a large institutional investor builds new rental homes as their own construction project (a "build-to-rent" community), those are exempt.

Renter protection resource. The law establishes a renter outreach resource to help renters of homes owned by large institutional investors navigate landlord disputes.

What this may mean for SWFL. Institutional single-family rental ownership in the Miami metro area is estimated at approximately 5% of single-family rentals. Southwest Florida is likely similar or lower. This means the direct impact on our specific market is modest but real. The primary place it may show up: Cape Coral tract-built homes and Lehigh Acres entry-price single-family homes, both of which have historically been categories where institutional buyers competed for cash purchases against traditional buyers. With those institutional buyers now restricted from adding to their portfolios, individual traditional buyers may face slightly less competition for those specific properties.

Provision 10. Whole-Home Repairs Act

The law creates federal grants and forgivable loans (loans you do not have to repay if you follow the rules) that help lower-income and middle-income homeowners and small landlords fix aging houses so those homes stay livable and stay on the market rather than deteriorating out of existence.

What this may mean for SWFL. Aging Cape Coral housing stock from the 1970s and 1980s. Older Fort Myers homes. Manufactured home communities. The federal grant and forgivable loan money may help preserve inventory that would otherwise fall out of the usable housing pool. For the buyer market, that is preserved supply. For the current SWFL homeowner, that is potential access to home-improvement money.

Provision 11. RAD Cap Lifted by 100,000 Units

RAD stands for Rental Assistance Demonstration. It is a HUD program that moves aging public housing onto more stable funding so it can be renovated and preserved. The program previously had a cap on how many apartment units it could cover. The ROAD Act raises that cap by 100,000 units and adds new tenant protections.

What this may mean for SWFL. Public housing inventory in Lee and Collier counties is not enormous, but it exists. The RAD expansion may allow local housing authorities to renovate and preserve units that would otherwise be at risk of losing federal funding entirely.

Provision 12. VALID Act and Appraisal Modernization (UAD 3.6)

Two related items in the appraisal category.

The VALID Act (Veterans Affairs Loan Informed Disclosure Act) requires clear side-by-side comparisons of Veterans Affairs (VA) loans versus Federal Housing Administration (FHA) loans so that veterans buying homes can make informed decisions between the two federally-backed loan options. This directly benefits every SWFL veteran buyer we work with, and it dovetails with the Hawley Team's veteran buyer expertise from our military family background.

Appraisal Modernization (UAD 3.6). The Uniform Appraisal Dataset is the standardized format appraisers use to value homes. Version 3.6 is the modernized update rolling out now. The goal is to make property valuations more consistent from one appraiser to the next.

What this may mean for SWFL. In a post-Ian market where appraisal consistency has been one of the friction points on the seller side (see our 6/25 First-Time Seller and 6/30 Halfway Mark posts), UAD 3.6 may help. The VALID Act specifically supports the SWFL veteran buyers who make up a real slice of our buyer file.

What This Means for Southwest Florida, Practically

Here is our honest read on which provisions may land most quickly in SWFL and which are more indirect.

Most immediate impact:

Small-Dollar FHA Pilot (Provision 7): Unlocks financing for entry-price manufactured homes and older condos that had been effectively cash-only markets. Could shift demand meaningfully in Lehigh Acres, N. Fort Myers, and some older Cape Coral inventory.

Large Institutional Investor 350-Home Rule (Provision 9): Reduces cash-offer competition for individual SWFL buyers on cookie-cutter Cape Coral tract homes and Lehigh Acres entry-price homes. Impact is real but modest given estimated 5% institutional share in the region.

VALID Act for Veterans (Provision 12): Directly benefits SWFL veteran buyers making comparisons between VA and FHA loans.

Meaningful indirect impact:

CDBG new construction authority + $1 Billion Innovation Fund (Provisions 2 and 3): Local governments now have more tools and more potential federal money for affordable housing initiatives. Whether they use them depends on local decisions.

NEPA streamlining (Provision 1): Faster HUD-funded infill projects across the SWFL urban footprints.

Modular housing reform + Whole-Home Repairs Act (Provisions 5 and 10): Cheaper new manufactured housing supply and preserved existing housing supply.

Neutral to limited direct impact on our specific market:

RAD cap expansion (Provision 11): SWFL has some public housing but not a large portfolio.

Bank investment cap raise (Provision 6): National banking mechanism; benefits SWFL indirectly through regional bank capital deployment.

Community bank formation (Provision 8): Could benefit SWFL over years, not immediately.

What We Do Not Yet Know

This law was signed one week ago. Federal agencies are still writing the implementation rules for most of these provisions. Specifically:

The Small-Dollar FHA Pilot has up to one year for HUD to design and launch. Actual small-dollar loan availability for SWFL buyers is likely 6 to 12 months away.

The CDBG new-construction authority requires updated HUD guidance, then updated local government plans, then actual project deployment. Realistic timeline: 12 to 24 months before we see actual new construction financed through this pathway.

The Institutional Investor 350-Home Rule applies to future acquisitions but the specific rule for enforcement and reporting has to be issued. Investors are watching the guidance closely.

The Innovation Fund grants will go through federal grant-application processes. First awards likely 6 to 12 months out.

What we are confident about: the direction of federal housing policy has shifted meaningfully. Whether the actual on-the-ground SWFL impact matches the headline potential depends on how these implementations roll out over the next 12 to 24 months. We will track it and report back.

Our Plan for the Next Two Weeks

The ROAD to Housing Act is too big for a single blog post to fully cover. Today's post is the overview. Over the next two weeks, the Hawley Team blog will publish a focused series of deeper-dive posts on the provisions most relevant to Southwest Florida:

The Institutional Investor 350-Home Rule and What It Means for Cape Coral Tract Homes (target: next week)

The Small-Dollar FHA Pilot: A Real Shot for SWFL First-Time and Manufactured-Home Buyers (target: next week)

The Supply-Side Bundle: NEPA, CDBG, RESIDE, Innovation Fund, and Modular Housing Reform (target: following week)

The VALID Act and Southwest Florida's Veteran Buyer Advantage (target: following week)

Send us a note if any of the 12 provisions is particularly relevant to a decision you are making right now. We are watching the implementation guidance as it rolls out and will report back as the specifics come into focus.

How We Can Help

If you are a SWFL buyer, seller, homeowner, or investor and you are trying to figure out what the ROAD to Housing Act means for your specific situation, send us a note. Kim and Martin will walk your specific property and financing situation against the 12 provisions and give you an honest read on what may change for you in the next 6 to 24 months, what may not, and what is worth watching.

Kim and Martin Hawley are Realtors with The Hawley Team at Keller Williams Fort Myers and the Islands.

The Hawley Team at Keller Williams Fort Myers and the Islands

(239) 420-9027 | martin@teamhawley.com | teamhawley.com

Disclosures

The 21st Century ROAD to Housing Act was signed into law on July 10, 2026 without the President's signature under the Constitution's automatic-enactment provision. The Senate passed the bill 85-5 on June 22, 2026. The House passed it 358-32 on June 23, 2026.

Provisions summarized in this post reflect the Hawley Team's reading of the law as of July 17, 2026, informed by our Keller Williams broker briefing, the Bipartisan Policy Center's issue brief, and public reporting from NPR, CBS News, CNBC, HousingWire, and several law firm client alerts. Specific implementation details will be established by federal agency rulemaking over the coming months and are subject to change. Nothing in this post should be construed as legal, tax, or financial advice. Consult a licensed attorney, CPA, or licensed mortgage professional for advice specific to your situation.

Neither the Hawley Team nor Keller Williams Realty takes any political position on the law's passage or on the President's decision not to sign it. This post is a substantive practical summary of the law as passed.

Each Keller Williams office is independently owned and operated. Equal Housing Opportunity.